Casutic Soda: A Market at a Crossroads

The global caustic soda (sodium hydroxide, NaOH) market, a foundational pillar of the international chemical industry, is navigating a period of profound and complex transition. The years leading up to 2025 have been marked by unprecedented volatility, with supply chain shocks, geopolitical tensions, and extreme energy price fluctuations creating a whipsaw effect on prices and production. As the market looks toward 2030, it faces a new set of structural realities. A dynamic of steady but modest demand growth is on a collision course with a constrained supply landscape, where new capacity additions are lagging. This fundamental imbalance points toward a progressively tightening market, sustained price elevation compared to historical norms, and a significant reshaping of global trade flows that will redefine regional competitiveness.

Caustic Soda Flake MarketThis comprehensive analysis, drawn from the “Global Caustic Soda Market Outlook 2025–2030,” delves into the intricate factors shaping this critical market. We will explore the baseline conditions established during the turbulent 2020-2024 period, dissect the key demand-side drivers across various industries, provide deep-dive analyses of supply-side dynamics in every major region, and present a multi-faceted forecast that includes baseline projections, alternative scenarios, and a watchlist of critical risks. For producers, consumers, and traders, understanding these interconnected trends is not merely advantageous; it is essential for strategic planning and navigating the opportunities and challenges that lie ahead in the evolving world of chlor-alkali chemicals.

Chapter 1: The 2020-2024 Baseline – A Foundation of Volatility

To comprehend the future trajectory of the caustic soda market, one must first understand the tumultuous baseline period from which it emerges. The years 2020 through 2024 were anything but stable, characterized by a global pandemic, a severe energy crisis in Europe, and a subsequent market correction that reset prices and trade flows.

The Pandemic Shock and Rebound: The onset of the COVID-19 pandemic in 2020 triggered a sharp contraction in industrial activity worldwide. Global caustic soda demand fell by an estimated 3-5%, effectively erasing several years of growth. Key consuming sectors like alumina, paper, and textiles saw significant downturns. The only bright spots were in water treatment and detergents, which saw resilient demand.

However, the market rebounded with surprising vigor in 2021 and into 2022. As industrial output recovered, demand for caustic soda snapped back. This recovery was met with a series of supply constraints that created a perfect storm for prices. Unplanned outages and hurricane-related disruptions in the U.S. Gulf Coast, a major production hub, took significant capacity offline. Simultaneously, China’s implementation of power rationing policies in late 2021 curtailed its output.

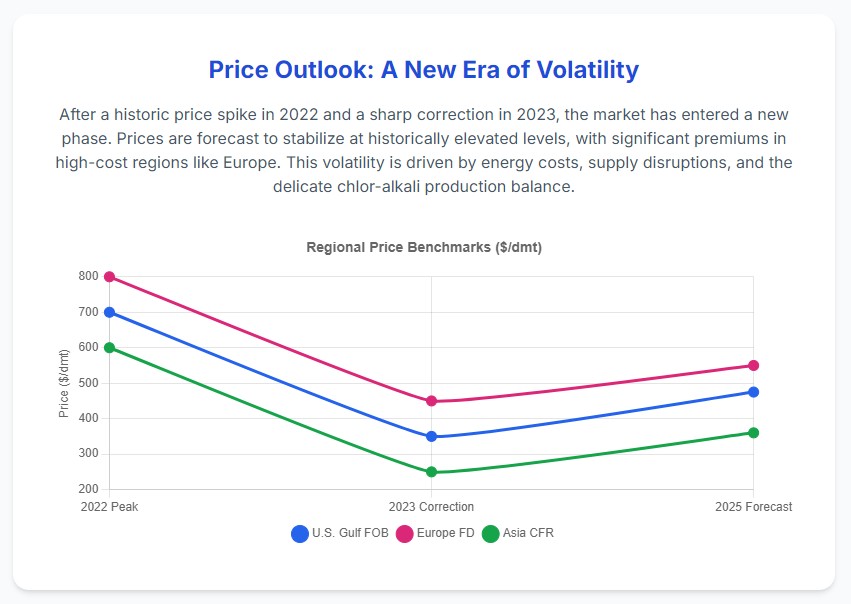

The European Energy Crisis and Price Super-Spike: The most dramatic factor was the European energy crisis of 2022. Spurred by geopolitical conflict and disruptions to natural gas supplies, European electricity prices skyrocketed to record levels. For the highly energy-intensive chlor-alkali process—where electricity can account for over 40% of production costs—this was catastrophic. Many European plants became uneconomical to run, forcing producers to slash operating rates to as low as 60-70% of capacity.

The impact was immediate and global. With European production severely curtailed, the continent flipped from being a self-sufficient market to a major net importer. This sudden demand for imports, primarily from the U.S., tightened the global market significantly. Prices soared to unprecedented heights. In the third quarter of 2022, European spot prices for caustic soda surged past $800 per dry metric ton (dmt), while U.S. Gulf export prices peaked above $700/dmt.

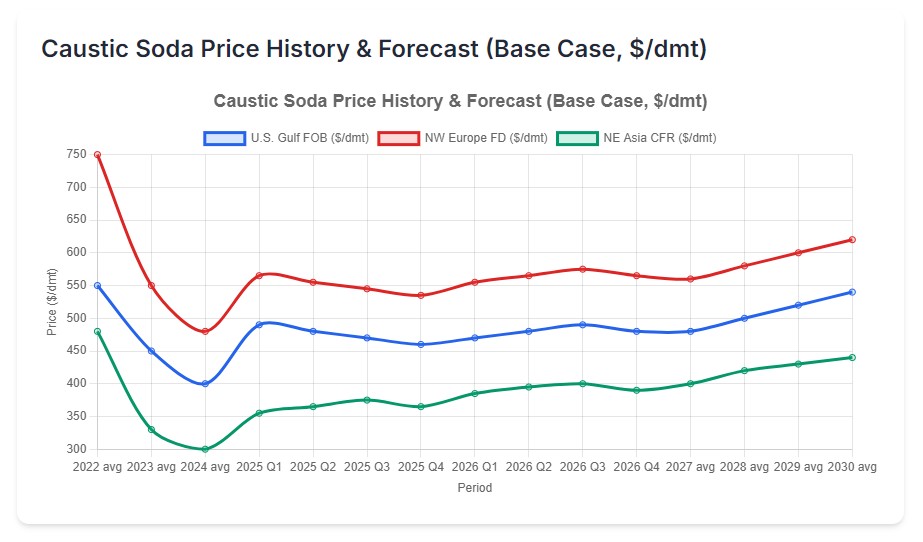

The 2023 Correction and Market Rebalancing: The extreme prices of 2022 were unsustainable and ultimately led to a market correction in 2023. European energy costs began to normalize, allowing local producers to partially recover their operating rates. Concurrently, the high prices and a broader economic slowdown led to demand destruction in some sectors and regions. Global demand growth slowed to near zero for the year.

This confluence of factors created a rare market surplus. By mid-2023, supply had lengthened considerably, and prices began a steep decline. U.S. export prices, which had been buoyed by the strong demand from Europe, fell from over $600/dmt in early 2023 to under $350/dmt by the end of the year. Asian prices bottomed out near $250/dmt amid weaker-than-expected demand from China. By the start of 2025, the market had found a new, more stable equilibrium, albeit at prices still above the pre-pandemic averages, setting the stage for the next phase of the market cycle.

Chapter 2: Demand-Side Drivers of Casutic Soda Market – The Pillars of Global Consumption

The demand for caustic soda is deeply embedded in the bedrock of global industrial activity. Its growth is not tied to a single application but is supported by a diverse portfolio of essential industries. Understanding the outlook for these key sectors is fundamental to forecasting overall market trends.

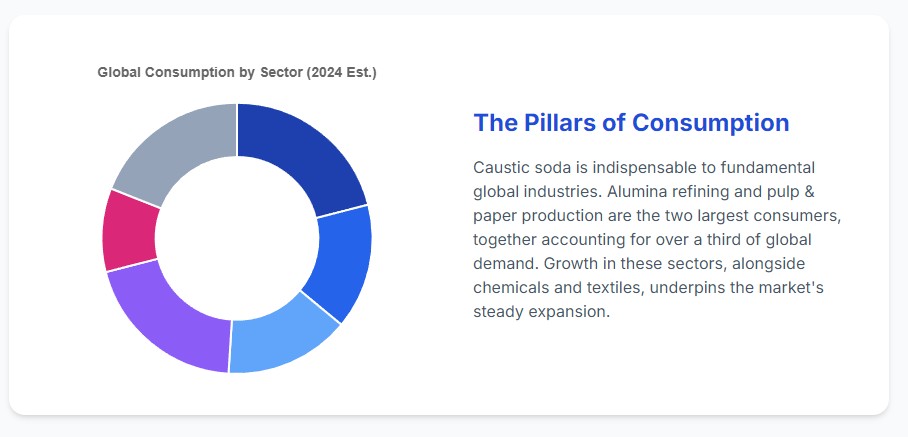

Alumina Refining: The Largest Consumer The single largest end-use for caustic soda globally is the refining of bauxite ore into alumina (aluminum oxide) via the Bayer process. This sector accounts for roughly 20-21% of total consumption. The connection is direct: for every ton of aluminum metal produced, about two tons of alumina are needed, which in turn consumes approximately 0.1 tons of NaOH.

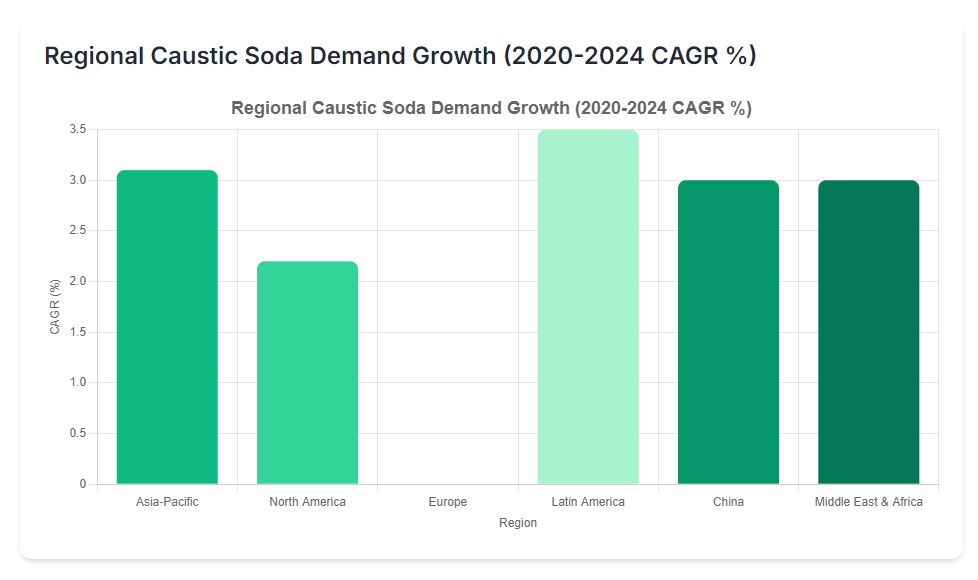

The long-term outlook for aluminum is robust, with demand driven by the global push for lightweighting in the automotive industry (to improve fuel efficiency and electric vehicle range), the growing preference for aluminum packaging (cans, foil) as a sustainable alternative to plastic, and construction needs in emerging economies. However, the growth in caustic soda consumption for this sector is not evenly distributed. China, the world’s largest aluminum producer, has capped its domestic smelting capacity, pushing investment into overseas alumina refineries in places like Indonesia and Guinea. This means that while global demand for alumina grows, the corresponding caustic soda consumption is shifting geographically to these new production hubs in Southeast Asia and Africa.

Pulp & Paper: A Tale of Two Markets The pulp and paper industry is the second-largest consumer, responsible for about 15% of global demand. Caustic soda is essential in the Kraft pulping process to digest wood chips and in bleaching sequences to achieve desired whiteness.

The sector is undergoing a significant transformation. While demand for graphic papers (newsprint, printing paper) is in secular decline due to digitalization, the market for packaging and tissue is booming. The rise of e-commerce has created immense demand for containerboard and cartonboard. Furthermore, a strong consumer and regulatory push away from single-use plastics is boosting demand for paper-based alternatives, from bags to food containers. This growth is most pronounced in Latin America, where major pulp capacity additions in Brazil are set to dramatically increase regional caustic soda consumption. In mature markets like North America and Europe, mill closures in the graphic paper segment are being partially offset by the resilient packaging sector.

Chemicals, Textiles, and Other Essential Uses Beyond the top two, a host of other industries rely on caustic soda:

- Organic and Inorganic Chemicals: This broad category, representing a combined 30-40% of demand, includes the production of solvents, propylene oxide, polycarbonates, and countless other processes requiring acid neutralization. In North America, it is the single largest end-use category.

- Textiles: Accounting for up to 10% of global demand, this sector uses caustic soda for mercerizing cotton to improve its strength and luster, and as a key reactant in the production of man-made cellulosic fibers like viscose/rayon. With a growing focus on sustainable fibers derived from wood pulp, the demand for viscose is rising, particularly in textile powerhouses like India and China.

- Soaps, Detergents, and Water Treatment: These sectors represent smaller but fundamentally stable sources of demand. Caustic soda is used in the saponification of fats to make soap and in the manufacturing of various detergent components. In water treatment, it is used for pH control and the removal of heavy metals, a segment poised for growth as environmental regulations tighten globally.

Crucially, for most of these core applications, there are no viable large-scale substitutes for caustic soda due to its unique chemical properties and cost-effectiveness, ensuring its continued role as an indispensable industrial chemical.

Chapter 3: Supply-Side Dynamics and Regional Deep Dives of Casutic Soda

The global supply landscape for caustic soda according to Istay Kimya‘s report is as complex and varied as its demand drivers. Production is concentrated in a few key regions, each with its own distinct cost structure, regulatory environment, and strategic posture. The interplay between these regions defines global trade and price setting.

North America: The Low-Cost Export Powerhouse North America, dominated by producers in the U.S. Gulf Coast, stands as the world’s preeminent low-cost supplier. This competitive advantage is built on two pillars: access to cheap and abundant natural gas from the shale revolution, which translates to low electricity costs, and vast, easily accessible salt dome deposits for brine feedstock. Major producers like Olin, Westlake Chemical, and OxyChem leverage these advantages to operate at a large scale.

With a production capacity of around 14-15 Mt, North America produces far more than it consumes domestically. This surplus makes the U.S. the world’s largest exporter, shipping over 5 Mt annually. The primary destination for these exports is Latin America, particularly Brazil, whose import needs are surging. The region’s producers have also adopted a “value-over-volume” strategy, demonstrating a willingness to idle capacity to support prices during downturns, which provides a floor for the global market. The primary risk to this region remains weather-related, with the constant threat of hurricanes disrupting production along the Gulf Coast.

Europe: The High-Cost Marginal Producer In stark contrast, Europe has become the world’s high-cost marginal producer. The region’s chlor-alkali industry is burdened by high electricity prices, which remain structurally elevated compared to other regions, and the escalating cost of carbon under the EU’s Emissions Trading System. The 2022 energy crisis starkly exposed this vulnerability, forcing widespread production curtailments and turning the continent into a major net importer of caustic soda.

European producers like INOVYN and Nobian are focused on efficiency and integration with downstream chemical production. However, they struggle to compete with imports from the U.S. or the Middle East on a cost basis. As a result, Europe’s role in the global market is that of a swing producer. When global prices are high, European plants run; when prices fall, they are the first to cut back. The region’s stringent regulatory environment, including a complete phase-out of older mercury-cell technology, further adds to the operational cost base.

China: The Global Behemoth and Market Pivot China is the undisputed giant of the caustic soda market, accounting for approximately 40% of both global production and consumption. Its capacity of nearly 50 Mt is spread across a fragmented landscape of state-owned and private enterprises. Many of these producers are integrated with the PVC industry, particularly in coal-rich inland provinces.

China’s cost structure varies significantly by region, from low-cost coal-based power in the west to more expensive grid power on the coast. The government’s “dual control” policies on energy consumption and intensity, along with periodic environmental crackdowns, can significantly impact production levels. China’s market position is pivotal; its domestic supply-demand balance determines whether it acts as a significant exporter to the rest of Asia or turns to the international market as an importer. In recent years, it has oscillated between these two positions, making it the key variable in the Asian market balance.

Rest of Asia, Middle East, and Other Key Regions

- Rest of Asia: This diverse region includes mature, export-oriented producers in Japan, South Korea, and Taiwan, which serve markets in Southeast Asia. India is a major growth story, with rapidly expanding demand from its textile and alumina sectors, coupled with new domestic capacity additions and protectionist anti-dumping duties. Southeast Asia is a key battleground, a net-importing region supplied by China, Northeast Asia, and the Middle East.

- Middle East: Benefiting from low-cost energy, the Middle East is an emerging export hub. Producers in Qatar, Saudi Arabia, and Oman are expanding capacity to serve both local industrial projects and growing markets in South Asia and Africa.

- Latin America and Africa: These regions are major net importers. Latin America’s demand is dominated by Brazil’s pulp and alumina industries, which are almost entirely reliant on imports from the U.S. Africa’s demand comes from mining, soaps, and water treatment, and is supplied by a mix of flake imports from Asia and liquid from Europe and the U.S.

Chapter 4: The Path to 2030 – Forecasts, Scenarios, and Strategic Imperatives

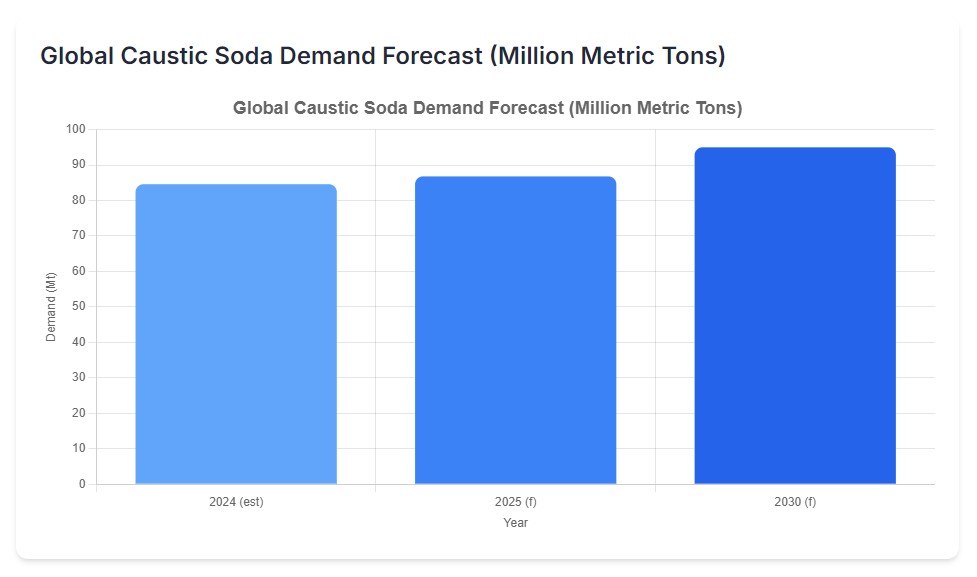

Looking ahead, Istay Kimya reports that the caustic soda market is projected to follow a trajectory of gradual tightening, but this path is fraught with uncertainty and potential disruptions.

Base Case Forecast: A Tighter, Pricier Market In our base case scenario, which assumes moderate economic growth and no major geopolitical shocks, the fundamentals point to a steadily tightening market. With global demand growing at ~2% annually and capacity expanding by only ~1%, global operating rates are forecast to rise from the low 80s to the high 80s by the latter half of the decade. An operating rate approaching 90% is near the practical maximum for the industry, leaving little cushion to absorb shocks.

This tightening balance is expected to keep prices structurally higher than the averages seen in the 2010s. U.S. Gulf export prices are forecast to stabilize in the $400-$500/dmt range, with European prices maintaining a significant premium and Asian prices trading at a discount.

Alternative Scenarios and The Chlor-Alkali Balance The base case is just one possible future. Several alternative scenarios could dramatically alter the market’s path:

- High Energy Cost Scenario: A repeat of the 2022 energy crisis in Europe would again force production cuts, leading to a surge in import demand and a spike in global prices.

- Global Recession Scenario: A significant economic downturn would hit key end-use sectors like construction and automotive, leading to a sharp drop in demand for chlorine and, consequently, caustic soda. This would create an oversupply situation and cause prices to fall toward the cash cost of production.

- China Rebound Scenario: Stronger-than-expected economic growth in China, combined with potential environmental closures of older plants, could quickly turn the country into a major net importer, absorbing global supply and driving prices higher.

A persistent wildcard in all scenarios is the chlor-alkali balance. Because in the report prepared by Istay Kimya, caustic soda is co-produced with chlorine in a fixed ratio, its supply is inextricably linked to the health of chlorine-dependent markets like PVC. A downturn in the construction sector can weaken chlorine demand, forcing chlor-alkali producers to cut operating rates. This, in turn, reduces the output of caustic soda, creating tightness and driving up its price, even if direct demand for caustic soda remains stable. This delicate balance is a constant source of potential volatility.

Conclusion: Strategic Imperatives for a New Era The global caustic soda market is entering a new era defined by tighter supply, heightened volatility, and a greater emphasis on regional cost advantages. For stakeholders across the value chain, adaptation and strategic foresight will be paramount.

- For Producers, the focus must be on operational efficiency, energy cost management, and disciplined capacity management. Low-cost producers in North America and the Middle East are well-positioned to expand their share of the export market.

- For Consumers, securing a reliable and cost-effective supply will be the primary challenge. This will require diversifying supplier portfolios across different regions, exploring longer-term contracts for baseload volumes, and investing in process efficiencies to minimize caustic consumption.

- For Traders, the persistent regional price spreads and potential for volatility will create significant arbitrage opportunities. Success will depend on agility, a deep understanding of logistical constraints, and a keen watch on the geopolitical and macroeconomic factors that can rapidly shift trade flows.

Ultimately, navigating the caustic soda market through 2030 will require a departure from the assumptions of the past. By preparing for a range of outcomes and understanding the fundamental drivers of supply, demand, and price, market participants can build the resilience needed to thrive in this dynamic and indispensable corner of the global chemical industry.

Istay Kimya is the leading supplier of caustic soda flakes from Turkey, trusted by industrial companies worldwide for consistent quality and reliable delivery. Visit our product page or contact us today to discuss your supply requirements.